How Much Does a Nursing Home Cost Without Medicaid?

Nursing home care can be expensive, especially when a family is paying without Medicaid. For many families, this becomes one of the biggest financial decisions they will ever face.

The cost of a nursing home without Medicaid depends on the facility, location, room type, level of care, and whether the stay is short-term or long-term. A private room usually costs more than a semi-private room, and facilities in higher-cost areas may charge significantly more than facilities in smaller towns or lower-cost regions.

Before choosing a nursing home, families should understand what private pay means, what may be included, what may cost extra, and what questions to ask before move-in.

What Does “Without Medicaid” Mean?

When a nursing home stay is paid without Medicaid, the resident or family usually pays through private resources.

This may include:

- Personal savings

- Retirement income

- Social Security income

- Pension income

- Investment accounts

- Family contributions

- Long-term care insurance

- Veterans benefits, if eligible

- Proceeds from selling a home

- Other private financial resources

This is often called private pay nursing home care.

Private pay does not always mean the family will pay forever. Some residents start as private pay while they apply for Medicaid, review long-term care insurance, use veterans benefits, or speak with an elder law attorney. Other residents remain private pay for the full stay.

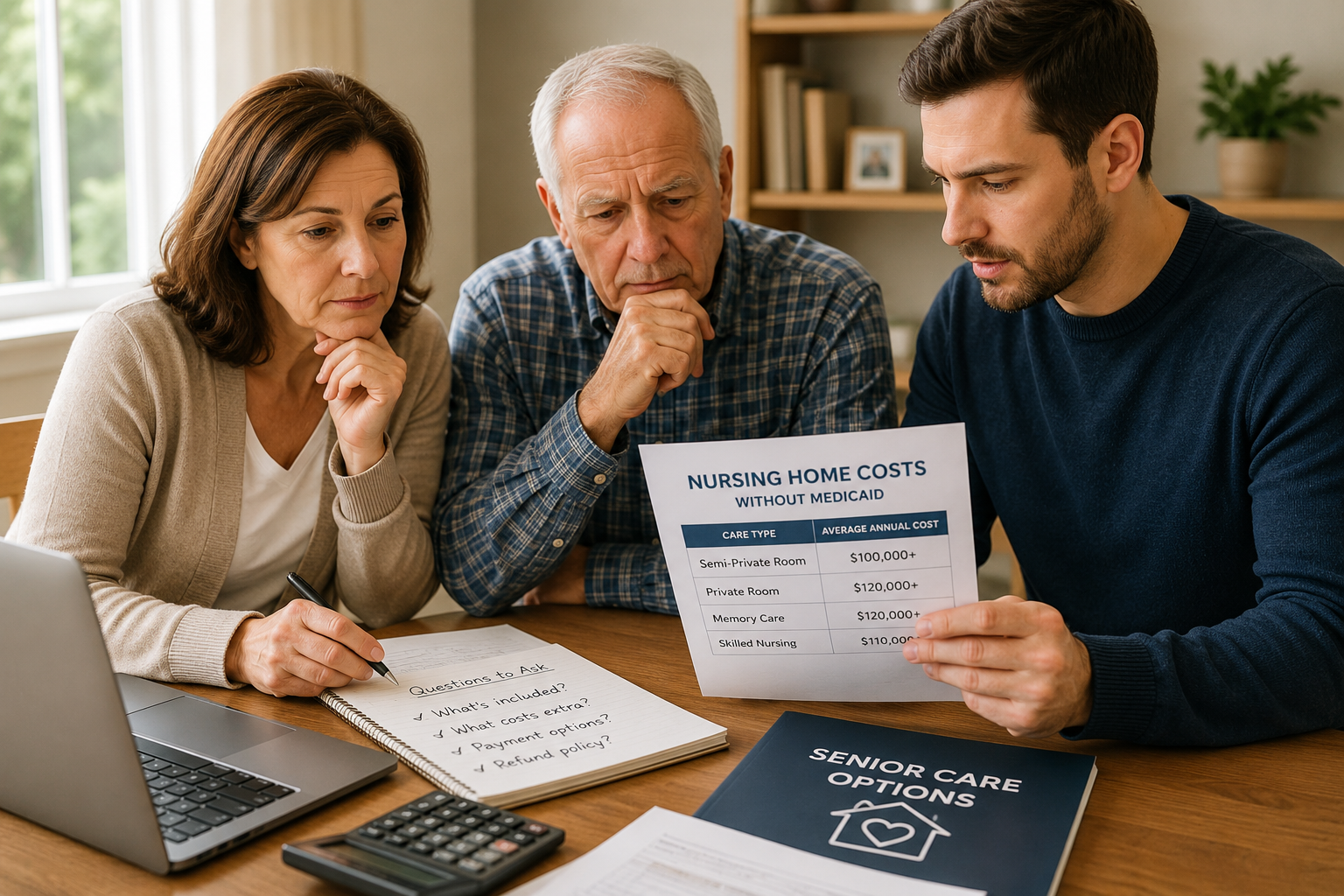

Average Nursing Home Cost Without Medicaid

Nationally, nursing home care often costs thousands of dollars per month. According to recent long-term care cost data, the national median cost for a nursing home semi-private room is over $100,000 per year, while a private room is higher.

That means many families should expect nursing home care without Medicaid to cost several thousand dollars per month, and often much more depending on the state, city, facility, room type, and care needs.

However, averages are only a starting point. The actual cost can vary widely.

A nursing home in one area may cost much less than a nursing home in another area. A semi-private room may be less expensive than a private room. A resident who needs more care may also have additional charges.

Families should always ask the facility for a written rate sheet before making a decision.

Why Nursing Home Costs Vary

Nursing home costs are not the same everywhere.

The price can depend on:

- State and local cost of living

- Facility reputation

- Room type

- Private room vs semi-private room

- Staffing levels

- Care needs

- Medical complexity

- Rehab services

- Memory care needs

- Location

- Amenities

- Ownership type

- Whether extra services are billed separately

A facility may advertise a base rate, but the final monthly cost may be higher if the resident needs additional care or services.

The most important question is not only:

“How much is the monthly rate?”

Families should also ask:

“What could cause the monthly cost to increase?”

Private Room vs Semi-Private Room

Room type is one of the biggest cost differences.

A semi-private room is usually shared with another resident. It is often less expensive than a private room.

A private room usually costs more because the resident has their own room. Some families prefer a private room for privacy, comfort, infection control concerns, or personal preference.

When comparing costs, ask:

- What is the cost of a semi-private room?

- What is the cost of a private room?

- Are both options available now?

- Is there a waitlist for private rooms?

- Can the resident switch room types later?

- Are there extra fees for room changes?

Do not assume the room type you want will be available immediately.

What Is Usually Included in the Cost?

Private pay nursing home costs may include many basic services, but every facility is different.

The monthly or daily rate may include:

- Room and board

- Meals

- Basic nursing care

- Help with bathing

- Help with dressing

- Help with eating

- Help with toileting

- Medication management

- Housekeeping

- Laundry

- Activities

- Basic supervision

- Care coordination

However, not every service is always included. Some services may be billed separately.

Families should ask for a written list of included services before move-in.

What Might Cost Extra?

Some nursing homes may charge extra for certain services, supplies, or care needs.

Possible extra costs may include:

- Private room upgrades

- Therapy services

- Pharmacy costs

- Incontinence supplies

- Medical equipment

- Specialty medical supplies

- Transportation

- Personal care items

- Beauty or barber services

- Special diets

- Higher levels of care

- Wound care supplies

- Oxygen or other medical support

- Room hold fees during hospitalization

These extra charges can make the total cost higher than the base rate.

Before signing an admission agreement, families should ask:

“Can you show me every possible fee that could be added to the monthly bill?”

Does Medicare Pay for Nursing Home Care?

Medicare may cover certain short-term skilled nursing facility care when specific requirements are met. This is usually connected to recovery after a qualifying hospital stay, illness, injury, or surgery.

That is different from long-term nursing home care.

If the person mainly needs help with daily activities like bathing, dressing, eating, toileting, supervision, or long-term custodial care, Medicare generally does not pay for that type of long-term nursing home stay by itself.

This is one reason families are often surprised by nursing home costs. They may assume Medicare will pay, but Medicare and long-term custodial care are not the same thing.

Families should ask the facility:

- Is this stay considered skilled nursing care?

- Is this long-term custodial care?

- Is Medicare expected to pay anything?

- If Medicare pays temporarily, when might that coverage end?

- What happens when Medicare coverage ends?

- What private pay rate applies after coverage ends?

These questions are especially important after a hospital discharge.

What Happens If the Family Cannot Afford Private Pay?

If the family cannot afford private pay long term, Medicaid may become part of the conversation.

Medicaid can help pay for nursing home care for people who meet financial and medical eligibility requirements. However, eligibility rules vary by state, and the process can be complicated.

Families should not wait until money is almost gone before asking questions.

Ask the nursing home:

- Does the facility accept Medicaid?

- Are Medicaid beds available?

- Can a private pay resident transition to Medicaid later?

- Is there a required private pay period?

- What happens if private funds run out?

- Does the facility help with Medicaid applications?

- What documents are usually needed?

- Are there services Medicaid does not cover?

Families may also want to speak with an elder law attorney or Medicaid planning professional before making large financial decisions.

Can Long-Term Care Insurance Help?

Long-term care insurance may help pay for nursing home care if the resident has a policy and meets the policy requirements.

However, every policy is different.

Families should ask:

- Does the policy cover nursing home care?

- What daily or monthly benefit is available?

- Is there an elimination period?

- How long does coverage last?

- What documentation is required?

- Does the facility help submit claims?

- Are assisted living or memory care also covered?

Do not assume a policy covers everything. Call the insurance company and ask for written benefit details.

Can Veterans Benefits Help?

Some veterans and surviving spouses may qualify for benefits that can help with long-term care costs. Eligibility depends on military service, financial situation, care needs, and program rules.

Families should speak with the Department of Veterans Affairs, an accredited veterans benefits advisor, or another qualified professional before assuming benefits are available.

Ask the facility:

- Do you work with veterans benefits?

- Do you accept residents using VA-related benefits?

- Can you provide documents needed for a benefits application?

- Are there nearby VA resources that may help?

Veterans benefits can be helpful, but they may not cover the full cost of nursing home care.

Questions to Ask Before Paying Privately

Before choosing a nursing home without Medicaid, families should ask detailed financial questions.

Important questions include:

- What is the daily rate?

- What is the monthly estimated cost?

- Is the rate different for private and semi-private rooms?

- What is included in the rate?

- What costs extra?

- How often can rates increase?

- How much notice is given before rate increases?

- Is there a deposit?

- Is there an admission fee?

- Is there a minimum stay?

- What happens if the resident goes to the hospital?

- Is there a room hold fee?

- What happens if the resident needs more care?

- Can the resident convert to Medicaid later?

- Does the facility accept long-term care insurance?

- Does the facility work with veterans benefits?

- Who explains the admission agreement?

- Can the family review the agreement before signing?

These questions can help families avoid surprises after move-in.

Compare More Than Cost

Cost matters, but it should not be the only factor.

Families should also compare:

- Quality of care

- Cleanliness

- Staff communication

- Safety

- Food quality

- Activities

- Location

- Visiting convenience

- Memory care support

- Rehab availability

- Medical support

- Family reviews

- State inspection information

- Long-term fit

The least expensive facility is not always the best fit. The most expensive facility is not automatically the best either.

The right choice is the facility that can meet the person’s needs safely, clearly explain its costs, and fit the family’s financial plan.

Get Advice Before Making a Major Financial Decision

Nursing home care can affect savings, income, home ownership, Medicaid eligibility, taxes, estate planning, and family responsibilities.

Before making major financial decisions, families may want to speak with:

- An elder law attorney

- A financial advisor

- A Medicaid planning professional

- A long-term care insurance specialist

- A veterans benefits advisor

- The facility billing office

- A hospital discharge planner, if applicable

This article is general information and is not legal, financial, medical, or insurance advice.

Next Step

Nursing home care without Medicaid can be expensive, but families have options to compare. The key is to understand the real monthly cost, what is included, what may cost extra, and what happens if the resident’s needs or finances change.

Nursing Home Placement helps families browse nursing homes, assisted living communities, memory care, rehab, retirement communities, and skilled nursing options by location and care type.

Start by browsing senior care communities near you, or use our Get Help Finding Care form if you need help narrowing down the right option for your family.